By MITCH ZACKS

In 2019, total earnings (or aggregate net income) for S&P 500 companies was expected to be down -1.5% on +3.1% higher revenues. The takeaway is simple: corporations made less profit in 2019 compared to 2018.

Even still, the S&P 500 index was up +31.49% over the same time frame. Many readers are probably noticing the flaw in the logic here: corporations do a little worse year-over-year, but the stock market surges. What’s wrong with this picture?

Actually, there may not be anything wrong with this picture at all. Markets move on a variety of factors – interest rates, monetary policy decisions, but perhaps most importantly, how expectations match up against reality. 2019’s stellar year can be explained by taking a closer look at these other factors, in my view. Here are our three takeaways.

1. Follow the Money

I believe investors should not underestimate the influence that “lower for longer” interest rates can have on equity prices. With investors starved for yield and interest rates seemingly anchored to near-zero levels, any indication of monetary policy easing generally results in a “risk-on” environment.

In 2019, the Federal Reserve lowered interest rates three times (thereby reversing all of the 2018 rate hikes), and they engaged in quantitative easing-like actions by purchasing $60 billion in Treasuries per month and stepping in to fund overnight lending through the repo market. Globally, the European Central Bank, the Bank of Japan, and the People’s Bank of China all implemented accommodative policies.

With strong economic fundamentals in the backdrop, easy money is almost always a tailwind for stock prices.

2. Zoom Out, and the S&P 500 is Actually Tracking Earnings

One of the main reasons that 2019 earnings looked so weak is that 2018 earnings were so strong, as a result of the tax cut. That made for very tough comparisons, and set a very high bar for corporations to reach.

But here’s the kicker: when you zoom out and look at 2018 and 2019 earnings together, you find that earnings grew 23.2% in 2018 while declining -1.5% in 2019. Over that two year stretch, the S&P 500 rose approximately +24% – a nice balance between stock price appreciation and corporate earnings growth.

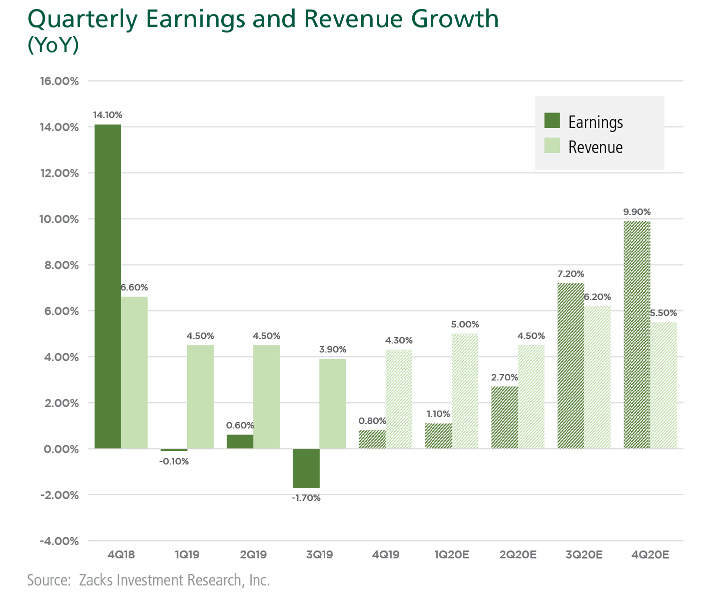

The picture emerging from the Q4 2019 earnings season – which also marked a strong rally for the S&P 500 – is one of steady improvement, with earnings growth on track to turn positive and an above-average proportion of companies beating top-line expectations. Estimates for Q1 2020 have come down, but they still compare favorably to other recent periods despite the coronavirus impact.

For Q4 2019 as a whole, total earnings for the S&P 500 index are expected to be up +0.7% from the same period last year on +4.3% higher revenues. Better-than-expected earnings per share (EPS) performance is a good explainer for the market’s rally.

3. Negative ‘Shocks’ That Aren’t So Negative

Many feared that the trade war with China would deliver significant blows to earnings and GDP, but the actual impact was arguably far softer than many feared. Global trade declined -1% for 2019 – which is rare for economic expansion years – but the US still managed to post modest but nicely positive GDP growth.

Wage gains outpaced inflation in the back half of 2019, and unemployment remains near historic lows. As long as the consumer remains in a relatively strong position, the US economy stands to benefit – consumer spending accounts for about two-thirds (68.1%) of the entire economy.7 The year ended with few signs of the consumer losing steam, with measures of consumer confidence remaining near cycle-highs.

Bottom Line for Investors

Earnings growth is expected to resume in 2020, with S&P 500 corporations projected to post +7.5% aggregate net income growth on +4.7% higher revenues.

Source: Zacks.com

The coronavirus may ding Q1 and Q2 earnings growth for China – and therefore the world – but the economic responses to virus-linked slowdowns have tended to be robust in history. We’d expect a strong bounce off the weakness, and I think investors should position for better-than-expected EPS performance throughout the year.

To help you get a deeper look into key economic indicators, earnings reports and other key factors that could influence the market, I am offering all readers our Just-Released March 2020 Stock Market Outlook Report.

Wenn du keinen Beitrag mehr verpassen willst, dann bestell doch einfach den Newsletter! So wirst du jedes Mal informiert, wenn ein neuer Beitrag erscheint!