By MITCH ZACKS

Equity investors should justifiably feel good and confident entering the new year. 2019 was a strong year for US and global stocks, and as it stands today the economy looks poised to add more growth in 2020 – with a rebound in corporate earnings to boot.

Since I’m about to give readers four reasons to expect more volatility in 2020, you might think I’m here to spoil the party. Quite the contrary! I think volatility is a good thing – it’s a normal, natural part of equity investing, and experiencing volatility from time to time means the market is functioning rationally, in my view. It is also important for investors to remember that volatility works both ways – delivering blows to the downside and triumphs to the upside over short periods of time.

When volatility happens, I think it’s almost always best to stay patient and let the volatility run its course. My advice in 2020 will almost certainly be no different.

Reason #1: We Can’t Ignore History

In a column late last year, I wrote that we should expect volatility in 2020 because history tells us we should. If you look at the S&P 500 over the last 38 years (1980-2018), 2 you’ll find that not only are corrections frequent, they’re the norm.

The average intra-year correction for the S&P 500 since 1980 is -13.9%. There are very few years in history where the S&P 500 didn’t fall at least -5% within the twelve-month period. In the last 38 years, it’s only happened twice: 1995 and 2017. In 2019, the biggest drawdown we saw was -7%, making it a below-average year for equity market volatility.3 In 2020, I think we’re due for a mean reversion, which might imply a correction more in tune with longer-term historical averages (-10% or more).

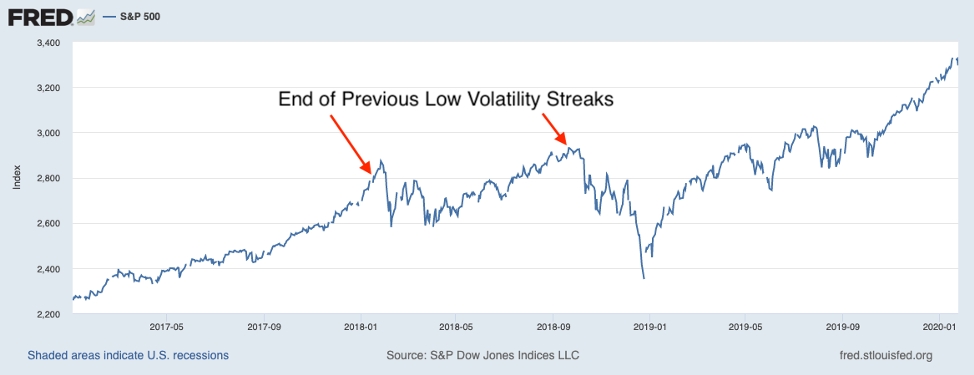

Reason #2: Low Volatility Generally Gives Way to High Volatility

Since the middle of October 2019, the S&P 500 Index has not moved 1% (or more) in either direction in a single day of trading. This low volatility streak is one of the longest the market has seen in 50 years, and it underscores the steady march higher that stocks have been on for months. History tells us that these extended periods of low volatility tend to give way to periods of high volatility.

The last time the low volatility streak happened for this long was just before January 2018 and October 2018,4 which marked the beginning of sharp corrections:

S&P 500 from 2017 – Present

Source: S&P Dow Jones Indices LLC5

Reason #3: Stock Buybacks are on the Decline

The windfall many corporations earned in the aftermath of the 2018 tax cut essentially went to one of three places: new investments, stock buybacks, or cash on the balance sheet. Stock buybacks are a corporation’s main tool for reducing outstanding supply of shares, therefore boosting existing shareholder value. From a supply – demand standpoint, lower supply means upward pressure on price, which is good for shareholders.

Since 2011 and particularly in 2018, the demand generated by stock buybacks was higher than demand by institutions such as mutual funds. In short, buybacks have been important. But early estimates show that stock buybacks were down approximately 15% in 2019, with more declines expected in the new year.6 Another factor to consider: fewer buybacks could mean a tougher road for corporation’s exceeding earnings per share targets, which could make investors jittery.

Reason #4: A Far from Straightforward Election Year

Election years have historically been good for stocks, and I think 2020 will be too. But I also expect some bumpiness given all of the unknowns with this particular election. When I say ‘unknowns,’ I’m not necessarily referring to the political outcome. I’m more concerned with foreign interference, contested results, civil unrest, and other extraneous factors that might lead to a period of political instability. I ultimately believe the nation will accept the result and move on, but I expect some choppiness in the build-up through November.

Bottom Line for Investors

It is worth repeating that volatility is a good thing for equity markets, and experiencing it – while often unsettling – is totally normal and expected. In my view, the S&P 500 is due for a correction this year on par with historical averages, in the –10% to –15% range. My hope is that long-term investors will keep the possibility of a market correction in mind this year, and remain calm and patient if (or when) volatility takes hold.

Wenn du keinen Beitrag mehr verpassen willst, dann bestell doch einfach den Newsletter! So wirst du jedes Mal informiert, wenn ein neuer Beitrag erscheint!